DPA One

Oct 15, 2025

An industry-leading platform redefining how America finds help to buy a home.

Executive Summary

When I inherited DPA One in mid-2022, the product was a stalled prototype designed by an external consultant. It aimed to centralize thousands of down payment assistance (DPA) programs into one accessible platform—but users were met with confusing forms and frequent “no results.” Over the next year, I led the redesign, data-population strategy, provider experience launch, and marketing rollout. Through continuous research, data-driven design, and strong collaboration with product and technology partners, DPA One evolved into an award-winning national platform. The redesign reduced search time by 3.5 minutes, boosted ease-of-use scores by +2.7 points, and achieved nearly 10× adoption growth, ultimately supporting Freddie Mac’s mission to make homeownership more accessible and equitable.

Background

DPA One was conceived to solve a fundamental problem in the U.S. housing ecosystem: information about down payment assistance programs was fragmented across thousands of state, local, and municipal websites. Loan officers, housing counselors, and borrowers often spent hours tracking down eligibility requirements and program details, with no easy way to compare options side-by-side.

By mid-2022, an external consultancy had produced a working prototype that captured the concept but not the experience. The interface required users to complete long, up-front forms before seeing results—often ending in frustration when the system returned “no matches.” Without a robust dataset or clear user feedback loops, adoption was low and confidence was lower.

I was brought in to reimagine the product experience, prepare the provider infrastructure, and build the foundation for a successful market launch.

Goals

Our design and product objectives were clear:

Centralize all DPA programs into one searchable, comparable experience.

Create trust and transparency by ensuring data accuracy and program completeness.

Design for two audiences: housing professionals as primary users, and borrowers as secondary but self-sufficient users.

Reduce friction and time required to find an eligible program.

Build provider engagement so the database would remain current and comprehensive.

Support Freddie Mac’s mission to reduce the cost of housing and increase equitable access to homeownership.

Discovery

We began by validating assumptions through both qualitative and quantitative research.

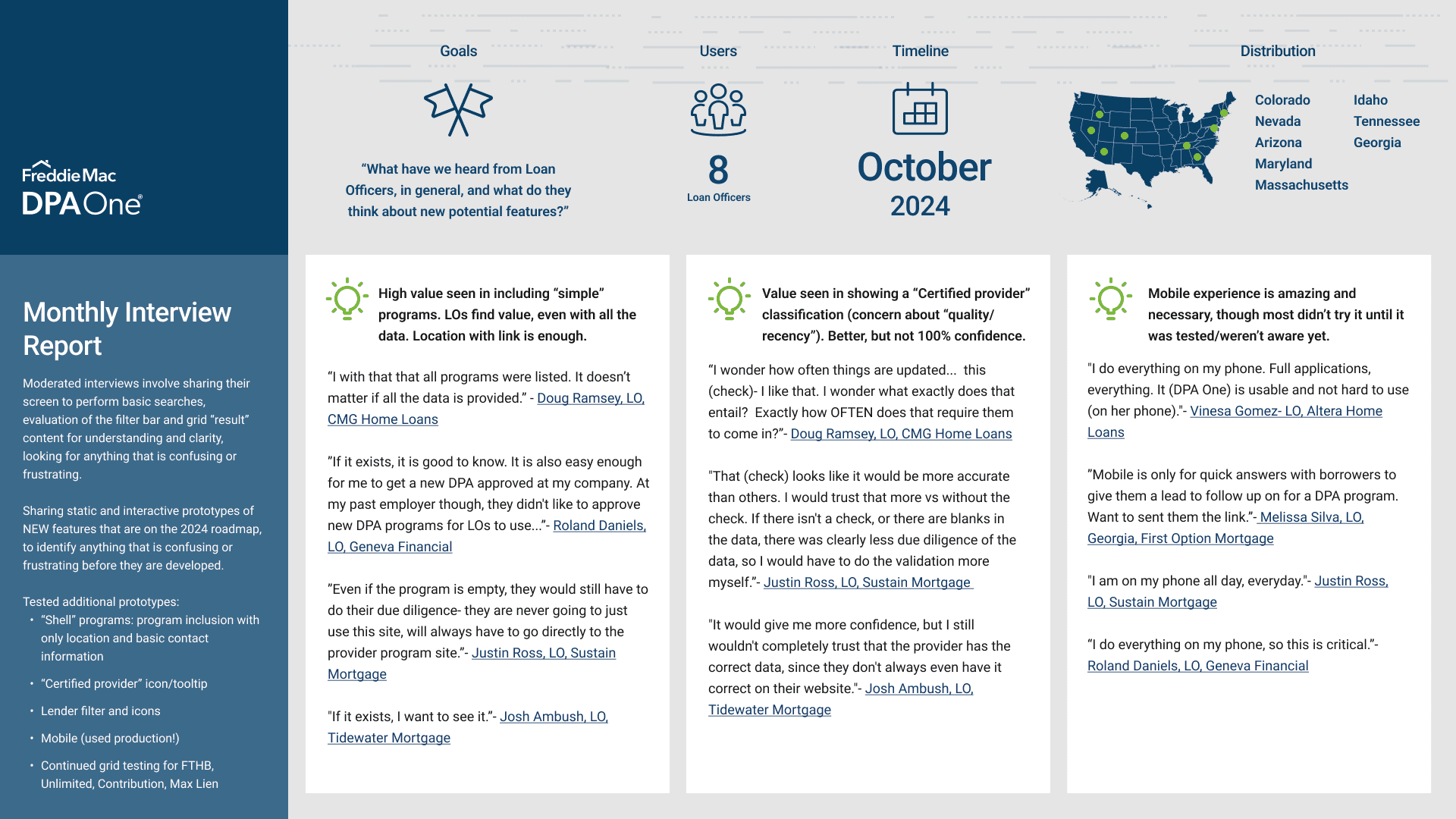

I conducted an average of six loan officer interviews per month and two provider interviews per month, supplemented with unmoderated usability tests of around 100 participants per round.

Early analytics via Google Analytics and Microsoft Clarity helped us understand real-world behaviors—what users searched for, how far they scrolled, and where they dropped off.

Here is an example of a monthly report:

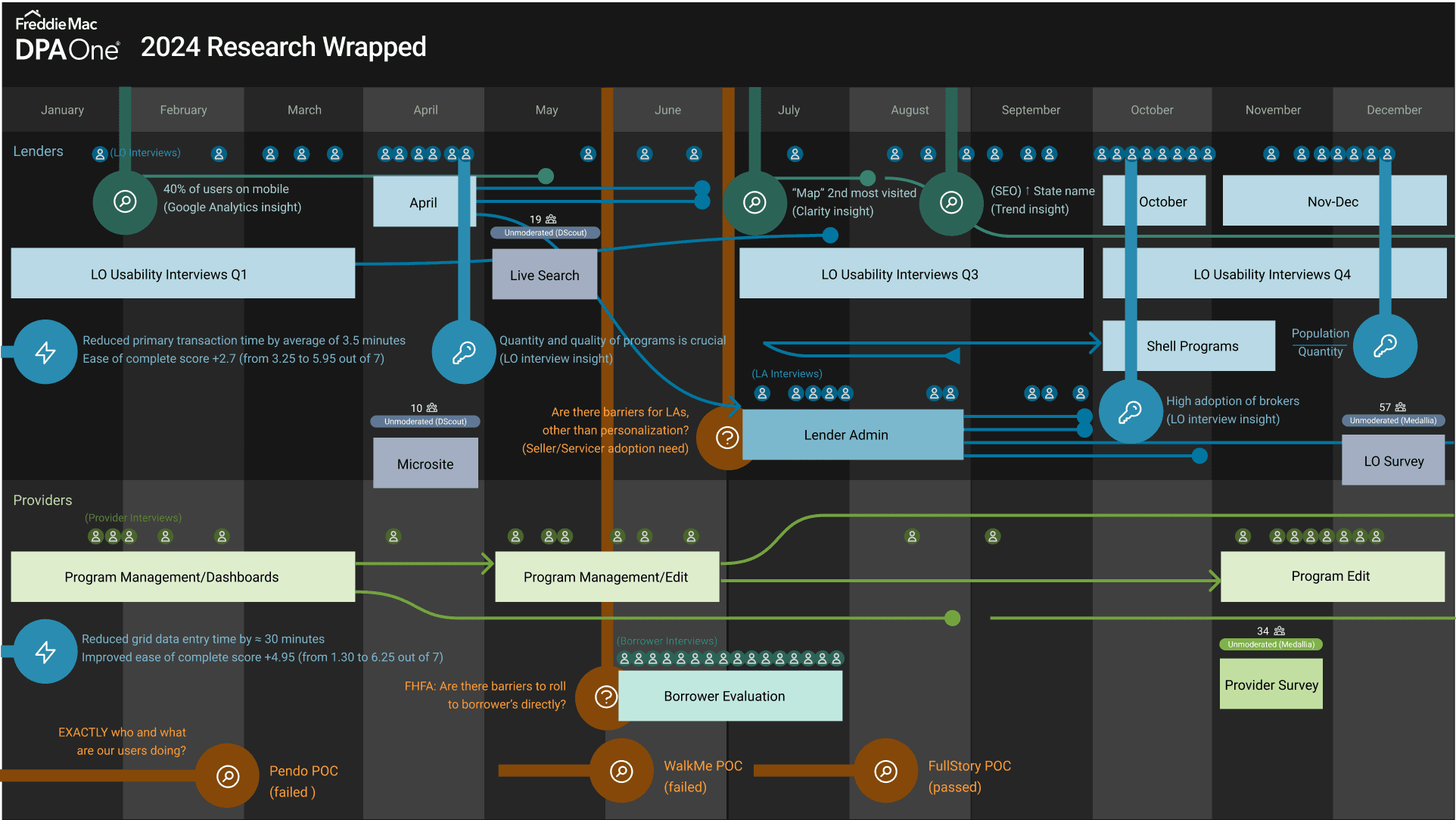

And this is an infographic for 2024 research reports based off of monthly interviews (qualitative), plus quantitative analysis from surveys, analytics, and google trends analysis, and analysis/POCs for new analytics software.

Key Insights

Users wanted to see everything, not nothing.

Starting with an empty search form gave no sense of scale or value. Users wanted to be impressed immediately by the breadth of available programs.Search behaviors varied by state.

States like Vermont or North Dakota had a handful of programs, making broad discovery easy. But states like California, Texas, and Florida had hundreds, requiring robust filters to narrow results.Data quality determined credibility.

Loan officers wouldn’t return unless they trusted the accuracy and completeness of the data. Providers, meanwhile, lacked time and resources to maintain it manually.

These insights informed a complete rethinking of the search experience and the provider engagement strategy.

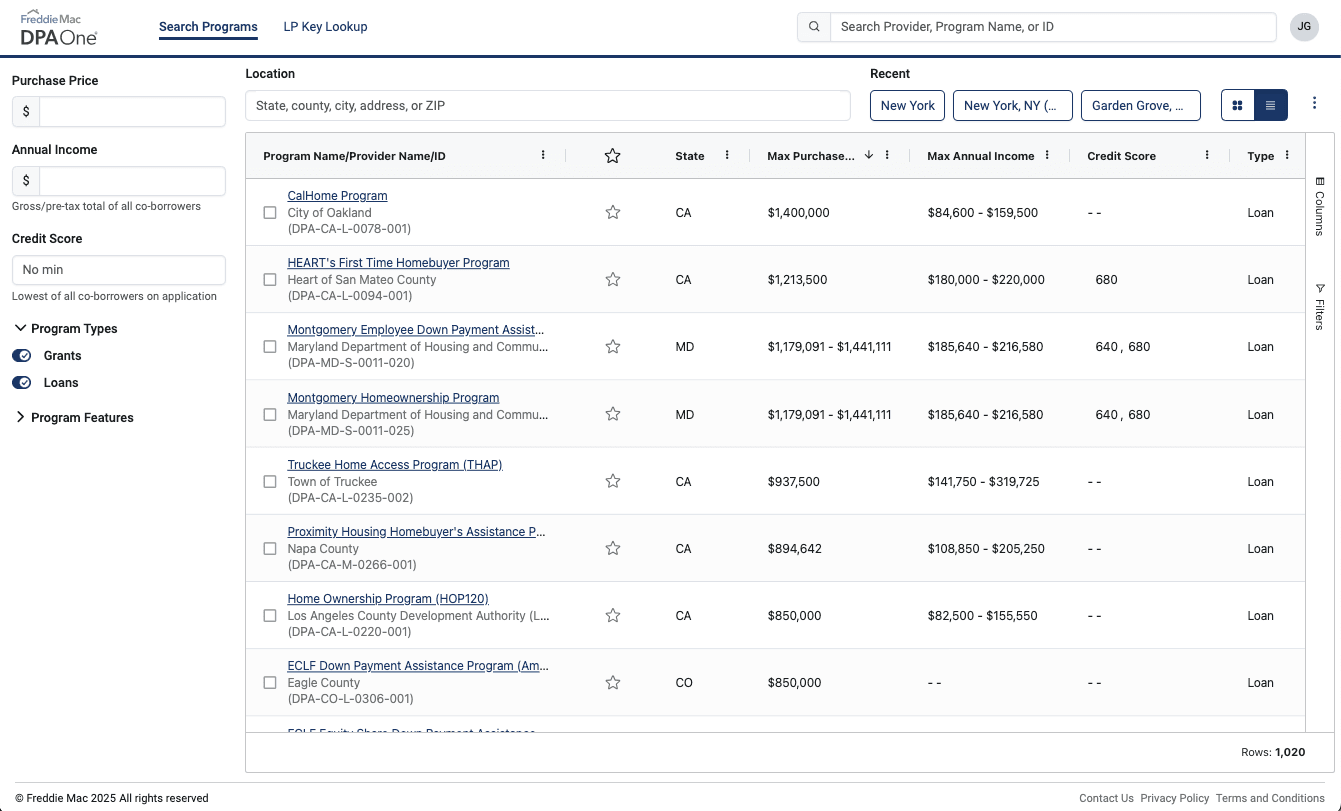

Redesigning the Search Experience

We moved from a form-first model to a filter-first model anchored by a data-rich results table. Users could view the full universe of programs upfront, then narrow results using filters such as location, borrower type, and loan parameters. Each column was sortable, enabling fast side-by-side comparisons.

This design change satisfied two key needs:

It created immediate trust by showcasing the platform’s scale.

It gave users multiple entry points—filtering, sorting, and scanning—to find relevant programs efficiently.

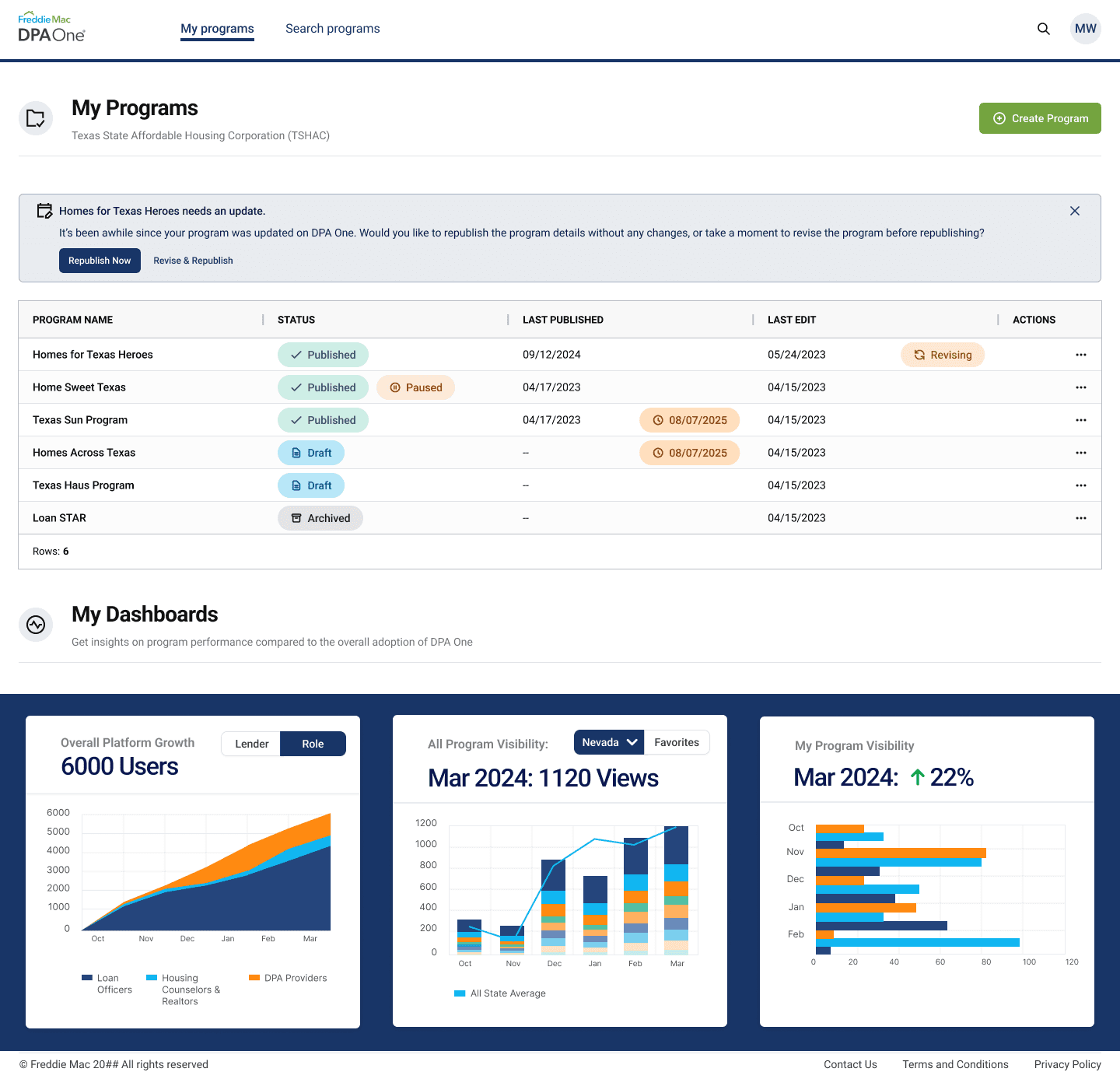

Building the Provider Experience

Because the platform’s value depended on data completeness, we built and launched a dedicated provider portal where DPA administrators could log in, manage, and update their programs directly.

To accelerate data population, I introduced AI-assisted scraping for municipal programs, automatically pulling verified data and reducing manual entry time for resource-constrained agencies.

Rolling Out and Marketing the Platform

We launched state by state, beginning with regions that had established DPA ecosystems. I designed the public marketing website to communicate the product’s value proposition and attract new users. Early behavioral data showed that both housing professionals and borrowers were searching at the state level, so we introduced dedicated state pages to improve SEO and drive registration.

This continuous feedback loop—research, design, analytics, iteration—created measurable improvements before full national release.

Outcomes

The redesign and rollout produced dramatic results within the first year and beyond:

Metric | Mid-2022 | Mid-2024 | Mid-2025 | Change |

|---|---|---|---|---|

Time on primary task | ~4.5 min | ~1 min | ~45 sec | – 4 min |

Ease-of-use (SUS 1–7) | 3.25 | 6.2 | 6.3 | +3.05 |

Net Promoter Score (NPS) | - | 85 | 91 | +8 |

Housing professionals registered | 24 | 5,400 | 9,000+ | +9,000 |

Provider participants | 4 | 550 | 800+ | +800 |

The combination of usability, transparency, and data quality directly contributed to industry recognition. DPA One received the HousingWire Tech100 Mortgage Award in both 2024 and 2025, acknowledging it as one of the most impactful digital innovations in the mortgage ecosystem.

Impact & Recognition

Beyond metrics, the project established a new standard for how affordability data can be designed, governed, and shared. It created a trusted national data hub that supports both the supply side (providers who manage program data) and the demand side (loan officers, housing professionals, and eventually borrowers).

Internally, the success of DPA One strengthened design’s strategic role within Freddie Mac. It demonstrated how a user-centered, data-driven approach could drive both mission outcomes and business efficiency. The platform now serves as a reference point for future digital transformation projects focused on housing equity.

Future Vision

The next evolution of DPA One is focused on:

AI-powered eligibility matching, allowing users to upload borrower profiles and instantly see qualifying programs.

Provider self-service tools for real-time updates and analytics dashboards.

API integration with loan origination systems to bring DPA data directly into lenders’ workflows.

Expanded borrower access, bridging the gap between professionals and first-time buyers.

These initiatives will deepen the product’s impact—making it easier than ever to discover and utilize financial resources that make homeownership possible.

Reflection

Leading the transformation of DPA One was a career-defining experience in marrying design, data, and mission. By championing usability, accessibility, and trust, we turned a struggling prototype into an award-winning national tool that empowers professionals and borrowers alike—and, ultimately, advances the goal of affordable homeownership for all.